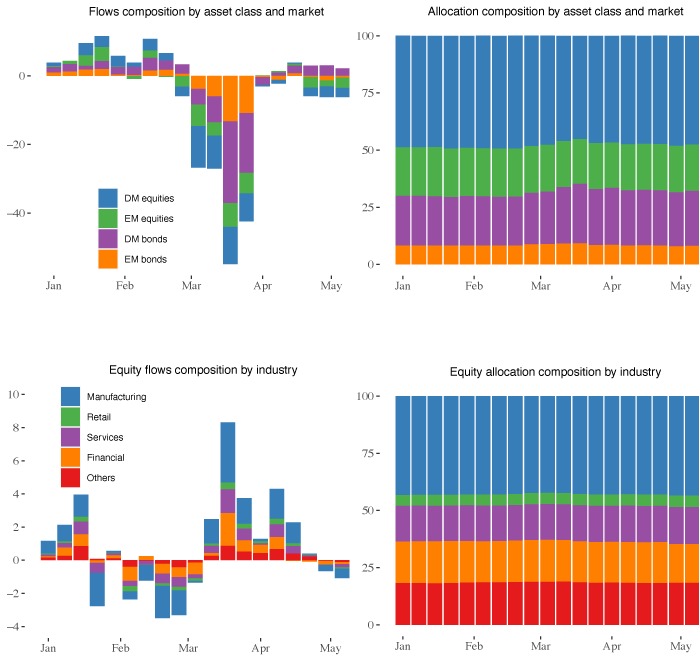

Compounding the global recession triggered by the COVID-19 pandemic, the worldwide health emergency also spurred a dramatic response in capital markets (Alfaro et al. 2020, De Bock et al. 2020). As investors gauged the economic consequences of the pandemic and the subsequent policy responses, they initiated a wave of capital reallocation between markets, asset classes, and industries. Figure 1 illustrates that this global shift in international portfolio flows was of historically large magnitude and that countries’ experience at the height of the episode differed widely. Figure 2 depicts the reallocation across markets, asset classes, and industries.

Figure 1 Densities of portfolio flows (% of allocation)

Figure 2 Composition of net portfolio flows (US$ billion) and allocation (% of total) across time, 2020

Notes: DM and EM stand for developed market and emerging market, respectively.

The heterogeneity across countries suggests that domestic pull factors have played an important role, standing in contrast to earlier risk-off events such as the global financial crisis and the taper tantrum. During these past events, the impact on portfolio flows was less dispersed across countries and largely determined by global push factors (among others Fratzscher 2012, Rey 2015, Avdjiev 2020). The question then arises as to whether individual countries’ handling of the crisis contributed to shaping the differing dynamics of portfolio flows.

In a recent paper (ElFayoumi and Hengge 2020), we use high-frequency data to address this question by evaluating international capital markets’ response to countries’ success, or lack thereof, in containing the pandemic and the key policy measures that governments enacted to limit the toll on public health and the economy. More specifically, we examine if and how the number of domestic infections, the stringency of the lockdown, and the fiscal and monetary policy response determined the magnitude of portfolio flows, market-implied sovereign risk, and stock prices during the COVID-19 pandemic.1 In addition, we explore four sources of heterogeneity based on market development (emerging vs. developed), asset class (bonds vs. equities), investors’ domicile (foreign vs. domestic), and industries.

The effect of infections and policy responses on capital markets

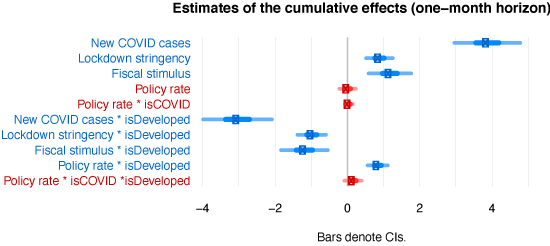

We build a panel dataset for 38 emerging and developed markets, with weekly information on the number of new COVID cases, the stringency of governments’ lockdown, and the fiscal and monetary policy response. We match these data with weekly portfolio flows from EPFR, spreads of sovereign credit default swaps (CDS), and stock prices. Our empirical approach relies on local projections (Jordà 2005) to estimate both the contemporaneous and the dynamic response over a one-month horizon.

We find that the domestic spread of the virus led to a cumulative increase in total net portfolio flows2 in emerging markets. This increase was associated with a reallocation towards safer assets as equity holdings declined and bond flows rose. Sovereign CDS spreads increased, suggesting that the increase in net portfolio flows was driven by demand for liquidity, potentially reflecting widening financing needs to mitigate the fallout from the pandemic (Figure 3).3

Our analysis also shows that, following an initial negative response, a more stringent lockdown led to larger net portfolio flows over the one-month horizon in emerging markets. Similarly, governments’ efforts to provide fiscal stimulus were successful in supporting higher portfolio flows to the domestic economy. Unlike the case for COVID infections, our results indicate that larger net portfolio flows in response to lockdown and fiscal stimulus measures were driven by an increased supply of financing, amidst stronger global demand for investment in safer asset classes. We do not find evidence that monetary policy actions in emerging markets played a role in the dynamics of portfolio flows. We interpret this finding in light of the dilemma hypothesis (Rey 2015), whereby US financial dominance renders emerging market monetary policy ineffective against market fluctuations.

Figure 3 Impact of domestic COVID cases and policy response on total net portfolio flows

In developed markets, the number of infections, the lockdown stringency, and fiscal stimulus do not appear to have played a role in driving net portfolio flows over a one-month horizon. Monetary policy loosening, in contrast, led to a decline in net portfolio flows – both for bonds and equities – as expected by interest rate parity. Interestingly, a reduction in rates triggered an increase in net flows upon impact, suggesting that monetary policy actions were successful in providing initial reassurance to markets.

Domestic-domiciled portfolio flows

The findings presented above focus on foreign-domiciled flows, that is, flows stemming from funds which are domiciled outside the recipient country. While foreign investors tend to be more diversified, domestic investors’ balance sheets are more vulnerable to countries’ idiosyncratic shocks due to their usually greater exposure to the local economy. This exposure adds an additional dimension to their response to domestic shocks, when compared to that of foreign investors (Caballero and Simsek 2020). Moreover, as Maggiori et al. (2020) point out, domestic investors are more likely to hold assets in local currency, which can amplify the effects of domestic fluctuations. In contrast, foreign investors allocate their funds in foreign-denominated assets, which offer them better insulation from local shocks and exchange rate fluctuations. We find evidence that domestic and foreign investors indeed responded differently to the spread of the pandemic, whereby domestic-domiciled total net portfolio flows declined in response to an increase in COVID cases, resulting in a higher share of foreign flows relative to domestic flows.

Impact of the lockdown across industries

The COVID-necessitated lockdown measures had a varying impact on economic activity across different industries, given their heterogeneous exposures to the related demand and supply factors, such as whether a product or service is considered essential and the extent to which the industry is reliant on global supply chains. Against our prior expectation, we find that the effect of lockdown measures on the retail sector was not particularly different from the financial and services sectors. All three sectors witnessed lower net portfolio flows in response to a more stringent lockdown, compared to the benchmark group.4 Net flows in the manufacturing sector, in contrast, increased strongly as the lockdown became stricter.

The role of policy measures for the global shock

In addition to their direct effect, domestic policy measures can also impact the dynamics of portfolio flows by mitigating or exacerbating the impact of the global shock. To quantify the importance of this channel, we estimate the effect of the interaction between the VIX – as a continuous measure of the global shock – and the lagged policy response. Our findings indicate that fiscal and monetary policy stimulus played an important role in attenuating the negative impact of the global shock both in emerging and developed markets. In contrast, more stringent lockdown policies may have amplified the negative impact of the global shock, particularly in developed economies.

Authors’ note: The views expressed are those of the authors and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

References

Alfaro, L, A Chari, A Greenland and P K Scott (2020), “Aggregate and firm-level stock returns during pandemics, in real time”, in Covid Economics 4: 2-24.

Avdjiev, S, L Gambacorta, L S Goldberg and S Schiaffi (2020), “The shifting drivers of global liquidity”, Journal of International Economics 125: 103324.

Caballero, R J and A Simsek (2020), “A Model of Fickle Capital Flows and Retrenchment”, Journal of Political Economy 128(6): 2288-2328.

De Bock, R, D Drakopoulos, R Goel, L Gornicka, E Papageorgiou, P Schneider and C Sever (2020), “Managing volatile capital flows in emerging and frontier markets”, VoxEU.org, 19 August.

ElFayoumi, K and M Hengge (2020), “Capital Markets, COVID-19 and Policy Measures”, in Covid Economics 45: 32-64.

Fratzcher, M (2012), “Capital flows, push versus pull factors and the global financial crisis”, Journal of International Economics 88(2): 341-356.

Gilchrist, S and E Zakrajšek (2012), “Credit spreads and business cycle fluctuations”, American Economic Review 102(4): 1692-1720.

Jordà, Ò (2005), “Estimation and inference of impulse responses by local projections”, American Economic Review 95(1): 161-182.

Maggiori, M, B Neiman and J Schreger (2020), “International Currencies and Capital Allocation”, Journal of Political Economy 128(6): 2019-2066.

Rey, H (2015), “Dilemma not trilemma: the global financial cycle and monetary policy independence”, National Bureau of Economic Research.

Endnotes

1 The analysis focuses on the domestic component of these variables, while controlling for global factors.

2 Total net portfolio flows are defined as the net value of purchases and redemptions of bond and equity funds.

3 Combined, information about the quantity (flows) and price (CDS spreads and stock prices) of assets provides an identification of the supply and demand channels of portfolio flows. To the extent that these two measures are tightly linked by market forces, shifts in supply are associated with changes in flows and spreads in opposite directions, whereas shifts in demand move both variables in the same direction. This intuition is in line with Gilchrist and Zakrajšek (2012) who study the relative contribution of credit supply and demand factors in corporate bonds.

4 The benchmark is the group of industries categorized into the sector “Others”.

More Stories

Capital Market Insights for Big Returns

The Future of the Capital Market

Capital Market Trends You Need to Know